It has been a long time, almost 20 years, since taxpayers have had to really think about it but, is a recession on the horizon? No one has a crystal ball, and many things can still happen, but we are starting to see some indicators that it might be just around the corner.

First, what is a recession. It is when there are two consecutive quarters of negative economic growth. During this period, which can last anywhere from months to even years, unemployment tends to rise quickly, and retail sales fall sharply. It’s all tied to consumer confidence.

How can that make sense when there is a labor shortage?

Hold-on, the global context is very different this time. Between this never ending pandemic, the war in Ukraine, gas prices, inflation, and an unreliable supply chain due to everything that is happening in Asia. We can no longer predict things like we had in the past.

How does this impact us individually?

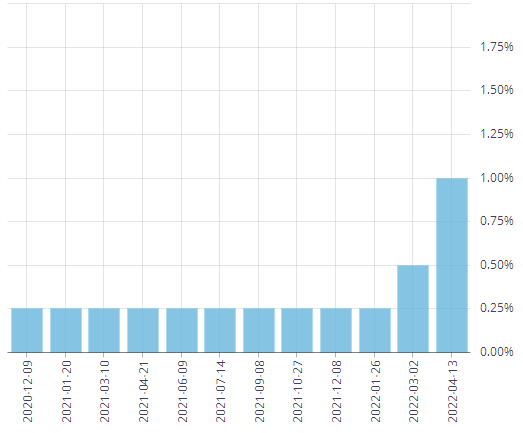

We just have to look at what is happening to interest rates. On April 13th, The Bank of Canada increased its policy rate by 50 basis points. This was the largest rate hike by the Bank of Canada since 2000. Is this Bank of Canada playing catch-up? Can it get the rate to where it wants to before a recession hits? If the Bank of Canada wins its race, will it be forced to then lower its rate to fend off a recession? Confusing, no kidding.

With these hikes, in turn, financial institutions have increased their variable mortgage rates. That’s no surprise. The two are interconnected. What is troubling though is the discount these institutions are now offering between their fixed rates and variable rates. Case in point, just weeks ago you could find a variable-rate mortgages at prime – 0.80% (P-.80%) or better.

Aggressive brokers are selling five-year fixed rates at 3.25% or less. That’s an unusually low 50 basis point premium to a variable. A spread that tight doesn’t come around often, and it makes you rethink all of the research suggesting variables are the way to go.

Research indicates that people have saved money on variable-rate mortgages on average 85% of the time. You would be crazy to switch to a fixed rate? Right?

What do the banks know that we don’t? Are they trying to get us to convert our variable rate mortgages into fixed ones? Should you?

When the interest rate curve flattens, it is an indicator that we are heading for a recession. See for yourself, currently there’s not much difference between a 5-year and 10-year fixed mortgage. This is an indicator, among others, of a looming recession.

Are you now totally confused, and do not know what to do. Call us at North East Mortgages, and we will sit down with you, and answer all your questions. We will take the time and work with you to determine what is the best financial scenario for you. Don’t wait, call us now.

Author:

Martin Spalding

Mortgage Broker